HIGHLIGHTS

- Dishman Carbogen Amcis Ltd., reported quarterly revenue (standalone) of ₹117 Cr for September 2024, marking an impressive year-on-year growth of 19.1%. It achieved a quarterly net profit of ₹14 Cr for September 2024, representing an extraordinary year-on-year growth of 346.5%.

- On a consolidated level, EBITDA margin came in at 18.8% for Q2 of FY25 compared to 10.8% for the same period last year.

- The newly validated facility in France is accelerating operations, contributing to the company’s growth. A significant contract exceeding €1 million was recently secured, raising the total order value to over €10 million.

INDUSTRY OUTLOOK

The Indian economy has demonstrated strength with a growth rate of 8.2%, positioning itself as the fastest-growing large economy in the past 2 years. The Indian pharmaceutical industry in the Indian economy has established itself as the 3rd largest producer of pharmaceuticals globally by volume. The significant segments of this industry include generic drugs, OTC medications, bulk drugs, and vaccines apart from CRAMS, i.e. Contract Research and Manufacturing Services. The world is fast moving towards outsourcing research and manufacturing services, and India is a world-favorite. CRAMS includes 2 significant components: Contract Research Services (CRS) and Contract Manufacturing Services (CMS). The global picture looks promising, as in 2022, the global CRAMS market was valued at about $202 billion, growing at a CAGR of 11%. Within this, CROs (Contract Research Organizations) are expected to grow at 10% CAGR

In comparison, CDMOs (Contract Development and Manufacturing Organizations) are set to grow faster at 14% CAGR from 2022 to 2027, pushing the overall CRAMS market to expand at around 13% CAGR during this period. The Indian CRAMS industry is set for strong growth, with a projected CAGR of 12.5% from 2022 to 2028, reaching a $50 billion valuation by 2028. This growth is driven by India’s cost competitiveness (30-40% cheaper than China), skilled workforce, shorter timelines for setting up facilities, and increased drug development and manufacturing collaborations. The Contract Research Organization (CRO) market is expected to grow significantly to $4.3 billion in FY27, fuelled by rising demand for late-stage clinical services. India’s favourable regulatory environment, cost-effective solutions, and increasing prevalence of chronic diseases position it as a key outsourcing destination for global pharmaceutical and biotech companies. Other prominent players in the pharma industry include Lupin Ltd., Zydus Lifesciences Ltd., Dr Reddy Laboratories Ltd., Sun Pharma, etc. These companies provide a varied portfolio of products and services in India and worldwide. The top 10 pharma companies have a market cap of approximately INR 1,35,300 crores. Outsourcing is becoming a global trend, and these companies have little exposure to CRAMS. Investment in CRAMS would generate profitability, given the scenario worldwide.

BUSINESS DESCRIPTION

Dishman Carbogen Amcis Limited (DCAL) is a prominent player in the global CRAMS industry, trusted by leading pharmaceutical innovators for its specialized and integrated solutions. From process R&D to late-stage clinical and commercial manufacturing, DCAL supports the entire drug development lifecycle, including the supply of APIs and intermediates. With a presence across the US, Europe, and Asia, DCAL serves major advanced markets and operates 10 state-of-the-art manufacturing facilities in Switzerland, India, China, the UK, France, and the Netherlands. Notably, its HiPo facility in Bavla, India, is among Asia’s most significant, enabling the company to capture high-margin opportunities in oncology and other high-potency compounds. The company operates through two key segments, seamlessly delivering comprehensive pharmaceutical solutions.

The CRAMS segment covers the entire drug development cycle, offering Contract Research Services for drug discovery and development and Contract Manufacturing Services for large-scale API and formulation production. The CRAMS segment, which makes up 82.9% of its total revenue, helps drug innovators develop and improve processes for new drug molecules at different stages. Once these molecules are approved, the company looks for large-scale commercial supply opportunities.

With services ranging from process development to clinical support and manufacturing, the company is well-positioned to grow and seize new opportunities in the global CRAMS market.

Complementing this, the Marketable Molecules segment focuses on producing and selling speciality chemicals and generic APIs, reinforcing the company’s integrated approach to serving global pharmaceutical needs. Under the Marketable Molecules segment, Dishman Specialty Chemicals produces highquality intermediates, fine chemicals, and quaternary ammonium compounds (Quats) used in catalysts, personal care, pharma intermediates, and disinfectants. Many products are GMP-compliant, with local stocks in Europe and the US.

Dishman also focuses on niche generic APIs, such as imaging reagents, with filed regulatory approvals and plans to expand their share in this segment. Additionally, the company targets the Vitamin D market, emphasizing its role in addressing health conditions caused by deficiencies.

FINANCIAL PERFORMANCE

Operations revenue has been trending since March 2021, with growth of approximately 12% for 2022 and 2023. Revenues have surged 8.41% in FY24. the company reported a net revenue of ₹2,615.77 crores compared to ₹2,412.92 crores in FY23. The CRAMS segment drove this growth with an 11.4% YOY increase, primarily due to a 14.8% rise in CRAMS CGAM revenue, supported by higher supplies of commercial molecules. However, CRAMS DCAL India’s revenue declined by 12.2% YOY. Revenue from the Marketable Molecules segment fell by 4.2% YOY, impacted by lower sales of quaternary compounds and generics, though partially offset by growth in Vitamin D analogues. The company invested ₹317.11 crores in capital expenditure during FY24, covering both growth and maintenance projects. Net debt, excluding lease liabilities, stood at ₹1,507.17 crores as of March 31, 2024, slightly higher than ₹1,458.37 crores the previous year.

The significant increase in inventory turnover from 0.706 to 2.52 indicates improved efficiency in managing inventory. The company is selling and replenishing its stock more frequently. The debtor turnover ratio improved from 4.09x in 2023 to 4.98x in 2024, reflecting enhanced efficiency in collecting customer payments. DCAL was able to convert its receivables into cash more quickly in 2024 compared to the previous year. As a result, a notable decrease in the working capital (WC) cycle from 52 days to 36 days indicates a significant improvement in the company’s operational efficiency.

The company’s strategic decision to take on additional debt highlights its focus on growth and expansion. The total debt-to-equity ratio has shown a measured increase over the last three years, rising from 0.256 in 2022 to 0.324 in 2023 and 0.360 in 2024, reflecting a balanced approach to leveraging financial resources. The investments in fixed assets, including new equipment and infrastructure, demonstrate a commitment to enhancing production capacity and operational efficiency. These forward-looking initiatives are expected to support higher sales and contribute to improved operating profits in the long run. While the interest coverage ratio has declined—from 0.925x in 2022 to 0.363x in 2023 and -0.0191x in 2024—it’s important to note that these changes align with the company’s growth phase, as it prioritizes long-term value creation. Furthermore, the stability in overall debt levels reassures investors that the company is not overreliant on debt, maintaining a prudent balance in its financial strategy. Cash flow from operating activity has increased compared to last year, which provides confidence in steady improvements in the company’s core business. DCAL has 0 promoter pledges, which reduces external risk and boosts shareholder confidence. With better management of assets and increased sales, the company could become profitable and increase stakeholder returns. In the previous FY, the management team led from the front, and neither member had an increase in their remuneration.

CURRENT DEVELOPMENTS AND FUTURE EXPECTATIONS

Financials – In the latest Quarterly numbers, the company clocked its highest-ever quarterly revenue, primarily driven by Carbogen Amcis- CRMS division and DCAL IndiaNCE APIs & Intermediaries. In Q2 FY25, DCAL reported strong financial performance with a year-on-year (YoY) growth of 34.5% in Net Revenue to ₹789 crores driven by increased commercial sales in Switzerland and India. The EBITDA number came in at ₹148 crores, among the highest in their history. The Cholesterol and Vitamin D analogues business done out of the Dutch facility showed a downtick in performance due to lower sales and higher input costs, but the company has proactively taken steps to reduce the input costs, and the benefits are expected to start accruing from Q4 this year. The company also expects to decrease its overall debt numbers by the end of the year.

The company has many subsidiaries outside India, and 90% of its sales are export sales, so managing foreign currency exposure is another critical area. Management of the company did pretty well on that metric in Q2 with a net positive charge of ₹227 crores in the bottom line. As DCAL is involved in a highly human capital-intensive business, employee benefit expenses become an essential metric to control and monitor. While there has not been any significant increase in QoQ numbers, the 6-month-ended numbers compared to last year have come in a tad higher at ₹636 crores from 578 crores.

Business and Future Expectations –

TThe company has been doing growth-related Capex for the past 2 years, and in the future, it expects to do mainly maintenance-related Capex, which will reduce the burden on the company. DCAL has also successfully navigated the EDQM issues at its Bavla site and is targeting to reach 30% EBITDA levels from its India operations. In the coming 2 years, the company’s management expects to lower its net debt to EBITDA levels from 3.2x to 1.5x-2x, which will be a welcome sign.

DCAL believes spending will increase the most in Oncology and Obesity areas by FY 2028 with a 5-year CAGR of 14% and 24%, respectively. As such, the company is focusing significantly on Oncology and currently has 15 molecules in Phase III, of which many molecules are in that segment only. DCAL has the largest HIPO facility in Asia at its Bavla site and is at the forefront of gaining from the high-margin HIPO opportunity in the Oncology space.

The company’s extensive facilities provide its competitive edge to win big longterm contracts, which will provide revenue visibility for the medium term. The current order book of Carbogen Amcis business stood close to a strong CHF 110 million, approximately 1000 crores. Delivering these orders profitably can develop confidence in stakeholders.

Recent events –

- Dishman Carbogen Amics Ltd. participated for the first time in Pharmtech & Ingredients, Crocus Expo, and Eurasia in Moscow and garnered interest from potential clients in Russia and CIS regions.

- Dishman Carbogen Amics Ltd. recently received the Choose France-Best Indian Investment in France demonstrating its progress in the healthcare industry and innovative capabilities.

- The company’s wholly owned subsidiary, Carbogen Amcis AG’s manufacturing sites in Switzerland, successfully completed USFDA inspections last year. The company’s Bavla site also successfully closed a similar inspection.

Strengths –

- With an investment of upwards of ₹1000 crores, the company has 25 largescale multipurpose manufacturing facilities, making it a suitable partner for many pharma companies and startups focusing on biotech.

- Globally, Dishman group has approximately 550+ scientists in its team, with 50% of its technical staff holding PhD degrees, which signifies massive human capital.

- The company has 4 decades of long-standing track record in CRAMS, APIs, and Specialty chemicals and solved complex problems for 250+ clients. It has also been approved and recognized by many health authorities worldwide.

- The company’s increasing net cash flow and substantial cash from operating activities reflect its robust operational efficiency and effective cash management.

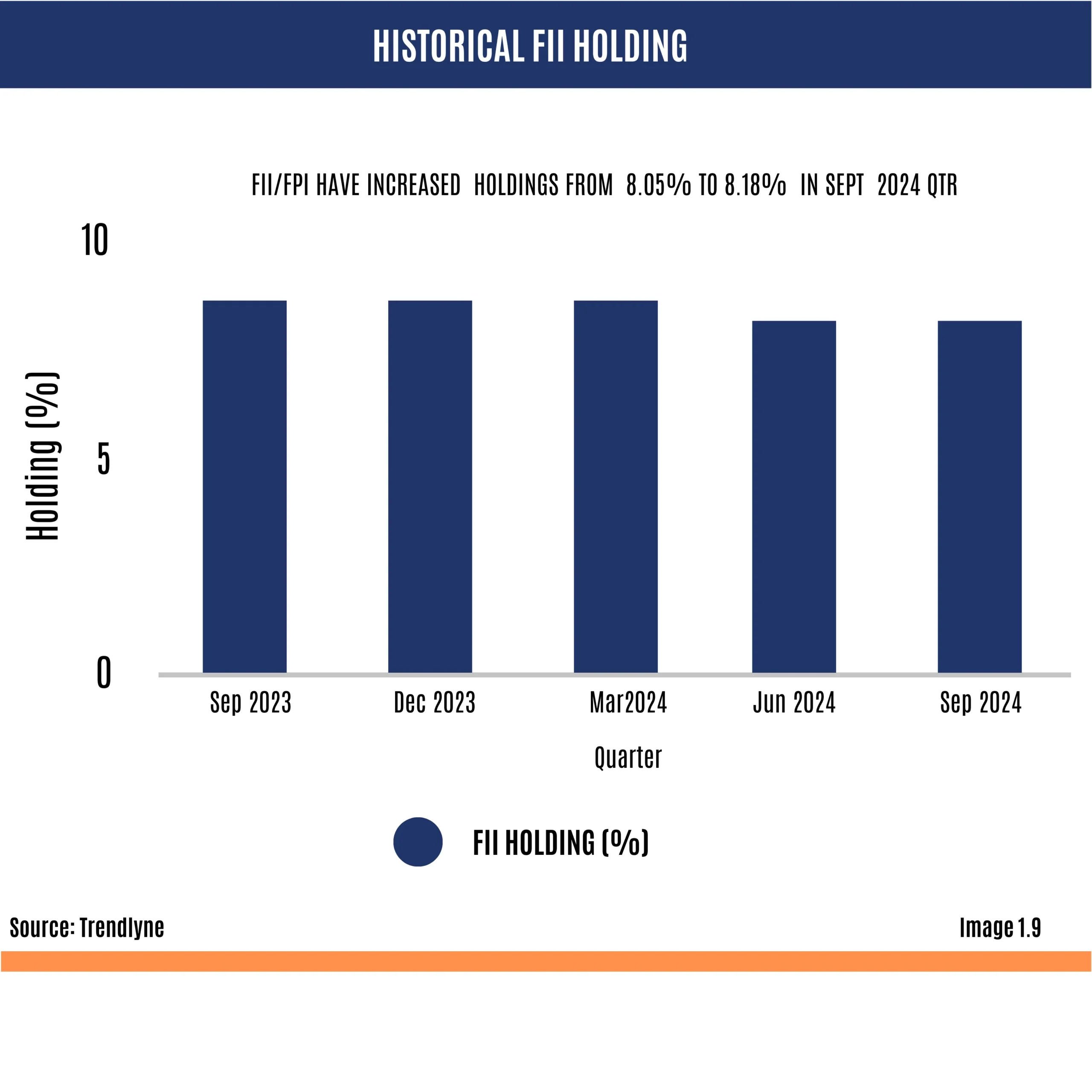

- The growing shareholding by Foreign Institutional Investors (FII), Foreign Portfolio Investors (FPI), or other institutions highlights their confidence in the company’s growth prospects and financial health.

- The company demonstrates a strong and healthy financial structure with a debt-to-equity ratio of 0.36, which is less than 1.

- DCAL made a 52-week high recently, on 11th December 2024, at 308 apiece.

CONCLUSION

The pharma sector and its allied industries have been a pillar stone for humanity and will remain one for the foreseeable future. The growth of the Indian pharma sector is on the uptrend and is slowly becoming a dominant force on the global front. The trend of outsourcing for specific research and manufacturing processes is increasing rapidly and is expected to reach 61% by FY 2030. DCAL has been in the industry for many decades, and with strong customer relations, it is well-positioned to take advantage of this trend. Having facilities in multiple continents and complex markets to crack, it is diversified and ably experienced to tackle the nitty-gritty of the pharma landscape. Having recently invested in a new facility and management’s focus to target small and mid-sized global biotech companies in the future, it is leaving no stone unturned to seize an opportunity. The company has also been focusing on growing segments like oncology for the past few years and can be a significant growth driver in the coming years. The barrier to entry in the company’s industry is relatively high, and with a future goal to improve margins and reduce debt, one can expect the company to do well.